Two Important Structural Shifts Shaping the Economy

The world economy is undergoing many secular changes, from the advent of artificial intelligence to de-globalization. Here, we look at two shifts occurring in the U.S. that will shape economic growth and policymaking for years to come

U.S. interest costs hit a post-WWII record in May.

One of the most frequently asked questions to hit our desk is around the U.S. budget deficit and the sustainability of the U.S. debt. As to the question of when deficits and/or debt begin to really matter, we’ve come to the conclusion that no one has a great answer. Accordingly, we went back into the historical data and found that it’s the interest costs of servicing the debt that actually matter for both financial markets and public policy. More specifically, we’ve identified that when interest costs hit 14% of tax revenue, a critical change occurs in Washington. When interest costs are below 14% of tax revenue, the U.S. government enters a regime of fiscal stimulus, which guided policy from 1995 to 2023. Conversely, when the interest cost exceeds 14% of tax revenue, the U.S. goes into austerity. In July 2023, that critical threshold was crossed and the 10-year Treasury raced from 3.7% to nearly 5.0% in three months until Treasury shifted to financing the deficit with shorter-term debt.

Last year, President Trump imposed one of the largest tax increases in American history by instituting tariffs to pay for an extension of tax cuts that were set to expire. We note this because the U.S. government was making progress on the deficit and rates before the Iran conflict began. But the conflict in Iran has set back some of that progress. Last month, net interest costs hit 19% of tax revenue, marking a new post-World War II high.

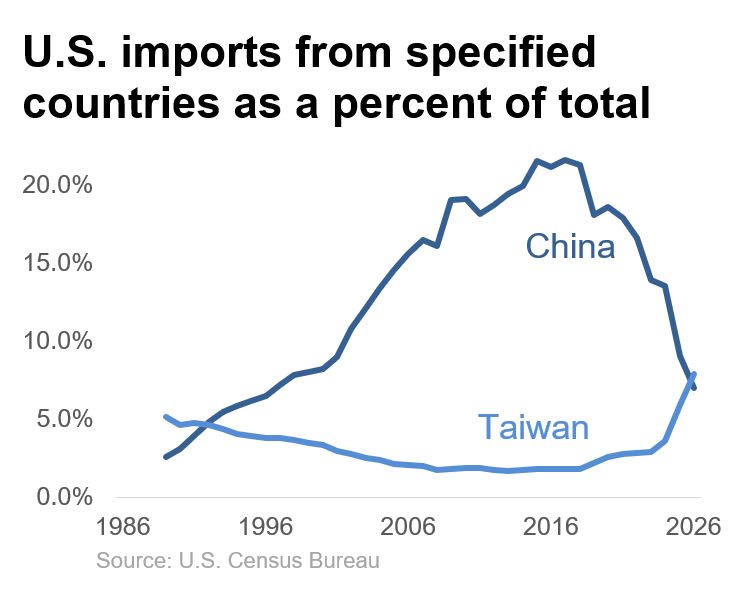

U.S. trading patterns are shifting rapidly under our feet.

We are not quite there yet, but by next month the U.S. will likely import more goods from Mexico than the E.U., more goods from Taiwan than China (right), and more goods from South Korea than Japan. This structural shift in U.S. trade patterns represents ongoing de-globalization, the push to bring supply chains closer to North America, and a need to wean the U.S. off China’s chokepoints. These trends do not account for transshipment, but are symbolic nonetheless. The shift toward a multipolar world that began a decade ago is now fully in motion. We see the Trump administration policy as a three-step effort: 1) Impose tariffs globally; 2) Incentivize domestic production; and 3) Fuel a weaker currency (akin to 20 years ago).

The first step is complete, with President Trump’s tariffs from last year getting things started and the full IEEPA replacement plan (in response to the SCOTUS ruling) likely to be in place by this summer. Step two is now in motion with Congressional passage of 100% expensing for capital expenditures, research & development, and factory building. But ultimately, we believe a weaker dollar will be necessary for reindustrialization to fully succeed.

Important Disclosures

Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index. Market and economic statistics, unless otherwise cited, are from data providers FactSet and Bloomberg.

This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation or solicitation to buy or sell any security. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry or security.

Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client. Investment involves risk. You should review the prospectus or other offering materials for an investment before you invest. You should also consult with your financial advisor to assist you with your analysis, risk evaluation, and decision-making regarding any investment.

The performance and other information presented in this communication is not indicative of future results. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies.

Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication.

Strategas Securities, LLC is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses. A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at https://researchdisclosures.rwbaird.com/. You can also call 1- 800-792-2473 or write: Baird PWM Research & Analytics, 777 East Wisconsin Avenue, Milwaukee, WI 53202.